India’s Industrial Growth Hits 5-Month Low

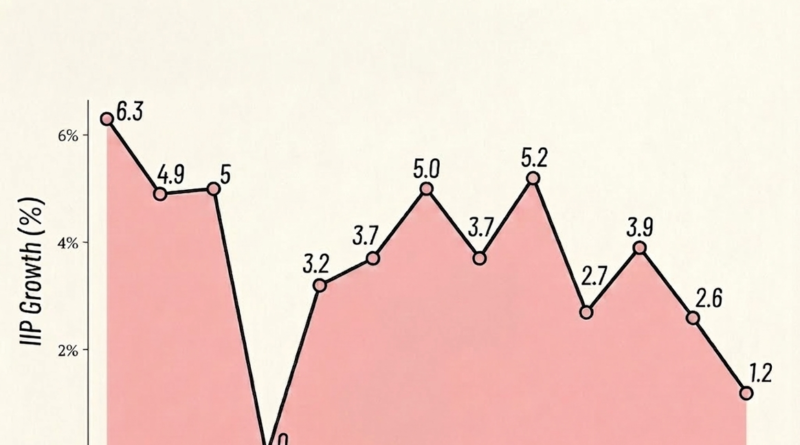

India’s industrial recovery faced a fresh hurdle in March 2026, as the Index of Industrial Production (IIP) growth slowed to a five-month low of 4.1%. This marks the first official data point reflecting the domestic impact of the West Asia crisis, which began in late February.

While the full-year growth for FY26 stood at 4.1% (slightly up from 4.07% in FY25), economists warn that the “deeper impact” of rising supply costs is yet to fully manifest in the production data.

The Core Sector Contraction

The 4.1% growth comes as a surprise to many, considering the Eight Core Sectors—which account for nearly 40% of the IIP—actually contracted by 0.4% in March.

“The 4.1% growth is impressive given that the core sector growth was negative for the month,” noted Madan Sabnavis, Chief Economist at Bank of Baroda.

Manufacturing Bears the Brunt

The manufacturing sector, the largest component of the IIP, slowed to a five-month low of 4.3%.

- Supply Chain Stress: Economists attribute this slowdown to the rising costs and tighter supplies of petroleum products and natural gas.

- Producer Sentiment: While the Purchasing Managers’ Index (PMI) remains in the expansion zone, it slipped in March, indicating that manufacturers are beginning to feel the heat of global uncertainty.

A Tale of Two Demands: Investment vs. Consumption

The March data reveals a sharp contrast in the Indian economy:

- Strong Investment (Capital Goods): Growth in capital goods surged to a 29-month high of 14.6%. This suggests that investment-led demand in the country remains robust despite global shocks.

- Weak Consumption (Consumer Goods): Consumer non-durables (everyday items) grew by a muted 1.1%. Even this small gain is attributed to a “low base effect,” as the sector had contracted significantly in the previous year.

Sector-wise Growth Breakdown (March 2026)

| Sector | Growth Rate | Note |

| Overall IIP | 4.1% | 5-month low |

| Capital Goods | 14.6% | 29-month high |

| Manufacturing | 4.3% | Hit by fuel costs |

| Infra & Construction | 6.7% | 9-month low |

| Consumer Non-Durables | 1.1% | Muted demand |

The Road Ahead

The Ministry of Statistics and Programme Implementation (MoSPI) data suggests that the slowdown actually began in January, pre-dating the West Asia conflict. However, experts from Crisil and Brickwork Ratings expect the “shockwaves” of the crisis to show up more clearly in the April-June (Q1 FY27) data, as weak producer sentiment and higher logistics costs take a firmer hold on the economy.